Curve Lending Overview

Curve Lending allows users to borrow crvUSD against any collateral token or to borrow any token against crvUSD, while benefiting from the soft-liquidation mechanism provided by LLAMMA. This innovative approach to overcollateralized loans enhances risk management and user experience for borrowers. Additionally, Curve Lending allows users to generate interest through lending (supplying) their assets to be borrowed by others.

Collateral in Lending Markets DO NOT back crvUSD

The collateral used in Curve Lending markets does not back crvUSD. All crvUSD within Curve Lending is supplied by users. Conversely, minting new crvUSD requires high-quality crypto collateral approved by the DAO. The crvUSD minting system is separate from the lending markets. See here for more differences between Curve Lending and minting crvUSD.

Curve Lending Risk Disclaimer

Full risk disclaimer on using Curve Lending can be found here

-

Borrowers

Borrowers are the ones borrowing assets. To do so, they create a loan and put up some collateral. In exchange for borrowing, they pay a certain Borrow Interest Rate (Borrow APY).

-

Lenders

Lenders supply their assets so they can be loaned to borrowers. To do so, they deposit their assets into a Vault. In exchange for supplying their assets, they are awarded a Lending Interest Rate.

Overview¶

Let's take a look at a single market to see the basics of how it works:

Let's breakdown the different entities and their roles in this market:

| Entity | Role | |

|---|---|---|

| Business Llama | Business Llama represents the lending market and smart contracts in the system. This llama uses CRV as collateral, and lends out crvUSD. Business Llama charges interest on crvUSD users borrow (Borrow APY), and pays interest to lenders who supply crvUSD (Lend APY). |

| Bob | Bob always thinks the market will crash, so he supplies his crvUSD and Business Llama lends it out and pays Bob interest (Lend APY). |

| Alice | Alice wants to go trade meme coins but doesn't want to sell her CRV, so she deposits CRV and uses it as collateral to borrow crvUSD. She feels safe knowing she's better protected here with LLAMMA and soft-liquidations than other lending markets. She is charged the Borrow APY on her debt while the loan is open. |

| Charlie & Daisy | Charlie and Daisy are just talking to the wrong Business Llama (lending market). All Curve Lending Markets are one-way, and isolated. They need to go and find the Business Llama that lends out CRV with crvUSD collateral. (Business llama with the red background here) |

Markets¶

There are many Curve Lending markets listed on the main UI. Each market uses a single type of collateral, and make loans in a single asset (all markets are one-way, and all markets are isolated). Some of the markets available are pictured below (we've used llamas in suits to illustrate different markets), but there are many more available, and new markets can be permissionlessly deployed by anyone, at anytime (as long as the asset has a suitable price oracle).

Note: All markets are paired with crvUSD. crvUSD must be either the collateral or the coin being borrowed.

Supplying (Lending)¶

Earning interest for supplying assets to Curve Lending is simple.

Let's have a look at an example where Bob lends his crvUSD for a year and how much he earns:

So after 1 year Bob earned 20 crvUSD and $20 worth of CRV, this equates to an APR of 40% over that year.

Depositing and Withdrawing¶

After depositing to a lending market your assets are added to the pool of available supply.

You can withdraw a supplied asset provided there are sufficient available (un-borrowed) assets in the market. For example in the below image Bob could have withdrawn up to 1200 crvUSD from the market, but he only withdrew 300 crvUSD.

If there are insufficient available assets for a full withdrawal, you can withdraw the maximum amount currently available. The high utilization rate will cause Borrow APY and Lend APYs to increase, incentivizing borrowers to repay their loans, and more lenders to supply. As available supply increases you can withdraw your remaining balance over time.

Supply Vault Share Tokens¶

By Supplying assets on Curve Lending, you are given Supply Vault Shares (more info here). These are tokens representing your share of the total supply. The value of these shares increases by Lend APY.

When you withdraw your supplied assets, the Vault Shares you had previously deposited are returned to the Lending Market. At this point, you receive the current value of the Vault Shares you are returning. This is how your interest on the supplied assets accrues. By withdrawing your assets, you effectively claim the interest that has been earned on your initial deposit during the time it was being lent out in the market.

Rewards APR¶

Rewards APR is a combination of CRV emission rewards and any other incentives provided to suppliers. Rewards accrue altogether and can be claimed at any time.

Rewards APR is ONLY given to Suppliers STAKED in the Liquidity Gauge

You MUST stake your Supply Vault Shares in the Lending Market's Liquidity Gauge to receive Reward APR.

You will not get any Rewards APR if you DO NOT stake. See here

For a market to have CRV rewards the following conditions must be met:

- The Curve DAO must vote to add a Liquidity Gauge to the

GaugeControllerfor that specific lending market - The liquidity gauge must receive a positive gauge weight through votes from veCRV holders. This will result in CRV being emitted to the liquidity gauge.

Due to the boosting mechanism of liquidity gauges, the Reward APR will be displayed as a range based on the user's boost factor. Learn more about boosting here.

Other incentives can be added by anyone, i.e., if a project wants to incentivize their token being used as collateral they may add incentives to a Lending Market. See here for more details and how to add them.

Borrowing¶

When borrowing from Curve Lending Markets, you are taking an overcollateralized loan against deposited assets (e.g., borrowing crvUSD with CRV collateral). In exchange, you are charged the Borrow APY on the borrowed assets.

Collateral is deposited into each lending market's LLAMMA system and split evenly across the chosen number of bands (N). Each band represents a small liquidation price range, with an upper and lower limit. If the oracle price enters one of your bands, soft-liquidation begins. Your loan is safe while the oracle price is higher than any of your bands.

See the image below for a breakdown of how supplied assets are borrowed, and how collateral is deposited into bands.

By minimizing the number of bands (N=4), you can maximize the amount you borrow (LTV), just like Charlie. Alice, however, prefers spreading his liquidity, so he chooses 10 bands (N=10) and does not maximize his borrowing. This explains why Charlie's loan is split into bands 3-12, while Alice's is split into bands 1-4. When you borrow, you can choose to split your collateral into any number of bands from 4 to 50.

There is no set rule for whether fewer or more bands are better. Different numbers of bands are better in different scenarios:

- More bands equate to having fewer losses in soft-liquidation, but this also widens your Liquidation Range, potentially extending the duration of soft-liquidation.

- Fewer bands will narrow your Liquidation Range, causing your collateral to be traded more aggressively, but you may remain in the Liquidation Range for a shorter time.

Soft-liquidation¶

Soft-liquidation begins if the oracle price of your collateral falls into one of your bands. At this point, your collateral will be linearly traded for your borrowed asset as the price continues to drop through each band.

Let's examine what soft-liquidation looks like in a simplified example with a single band in an ETH/crvUSD LLAMMA market. This example illustrates that if the price declines by 20% within the band, 20% of the ETH is converted to crvUSD. When the price is below the lower bound of the band (<$990), all the collateral is converted to crvUSD (100% crvUSD, 0% ETH). Conversely, when the price exceeds the upper bound (>$1000), all collateral remains as ETH (100% ETH, 0% crvUSD).

The below image represents multiple bands through soft-liquidation. Note the higher bands than the current price are fully converted to crvUSD and the lower bands are still ETH.

The value of traded assets remains as loan collateral throughout soft-liquidation. For example, if ETH is swapped for crvUSD, the value of that crvUSD is added to the collateral backing the loan. Additionally, LLAMMA works both ways; if prices increase through your bands, any swapped collateral will be traded back for your initial collateral (e.g., ETH swapped to crvUSD as the price decreased will be swapped back to ETH as the price increases).

Rebalancing collateral through soft-liquidation is incentivized for arbitrage traders by offering a small discount (when required) to buy or sell through LLAMMA. Trading back and forth your collateral is the reason why your health factor erodes over time during soft-liquidation. Higher volatility generally leads to greater losses. However, your losses are partly recouped by the earned trading fees for providing liquidity.

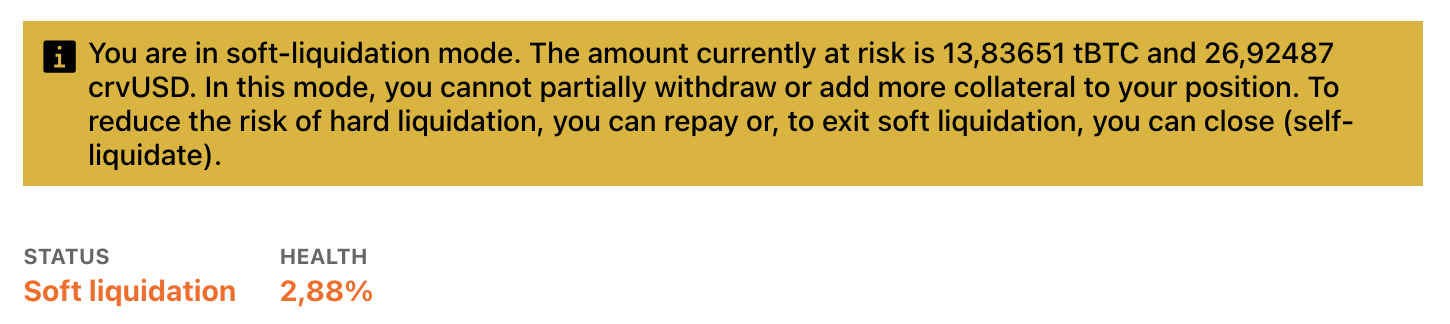

Collateral CANNOT be deposited while in soft-liquidation

Collateral cannot be deposited during soft-liquidation. Only debt repayment is allowed.

Health Factor & Hard-Liquidation¶

The Loan Health Factor is a measure of debt to collateral value. As long as the health factor is positive, the position remains open. The health of a loan decreases when the loan is in soft-liquidation mode and when debt increases due to interest paid.

Soft-liquidation losses do not only occur when prices go down but also when the collateral price rises again, resulting in the de-liquidation of the user's loan. This implies that the health of a loan can decrease even though the collateral value of the position increases.

It's even possible to be below your bands with all collateral converted to the borrowed asset (e.g., all CRV converted to crvUSD), while maintaining a positive health factor. If this happens, further price declines do not affect the position (e.g., all CRV traded for crvUSD, and crvUSD collateral covers debt and safety buffer).

A loan is elegible to be hard-liquidated if a the health factor reduces to 0. In a hard-liquidation, someone else can pay off a user's debt and, in exchange, receive their collateral. The loan will then be closed.

In contrast, most other lending platforms will hard-liquidate your collateral and terminate your loan if your loan falls below a minimum collateral ratio (LTV), even if only by a small amount for a brief time. This can be highly stressful for borrowers and lead to significant losses. Curve Lending offers a safer space and more peace of mind for borrowers.

Utilization, Lend APY and Borrow APY¶

The Lend APY and Borrow APY are based solely on the Utilization of the market. It is the ratio of assets supplied, to assets borrowed. In the image below the Utilization is 80% as 80% of the Supply is borrowed. Higher Utilization means a higher Lending APY and Borrowing APY.

For the current CRV Lending Market the Borrow APR for different Utilization rates is the following:

Difference between APR and APY

APRrepresents the Annual Percentage Rate (interest without compounding)APYis the Annual Percentage Yield (interest with compounding)

To convert the APR into APY, we need to annualize it and compound it every second (86400 seconds in a day):

Utilization Rate¶

The formula for Utilization is the following:

Borrow Rate¶

The borrow APR is the rate a borrower pays for borrowing out assets.

The formula for the borrow rate is as follows:

\(\text{rate}_{\text{min}}\) and \(\text{rate}_{\text{max}}\) values are obtained from the monetary policy contract of each Lending Market and are given in interest per second. We multiply the rate by \(365 \cdot 86400\) to get the APR because this is the amount of seconds in a year (\(365\) days \(\times 86400\) seconds in a day).

Lend Rate¶

Lend APR is the yield a lender receives in exchange for lending out their assets.

Formula to calculate the Lend APR:

More Information¶

For information relating to opening loans see the loan creation page

For information relating to how to supply assets see supplying assets page

For Frequently Asked Questions about Curve Lending see the FAQ here

For more technical information especially relating to the underlying smart contracts please see the Lending section within the Curve Docs